I am not privy to the innermost thoughts of Nick Thomas-Symonds, the Cabinet Office minister tasked with negotiating the “resetting” of our economic relationship with the European Union, but I can make a reasonable guess. While he feels he has to repeat the mantra about not rejoining the single market or the customs union, I doubt if in his heart of hearts he subscribes to it.

Last week he warned that British businesses trading with the EU face “more red tape, mountains of paperwork and a bureaucratic burden” if, God forbid, either the Tory party or the misleadingly named Reform party wins the next election and tears up Sir Keir Starmer’s “Brexit reset” deal.

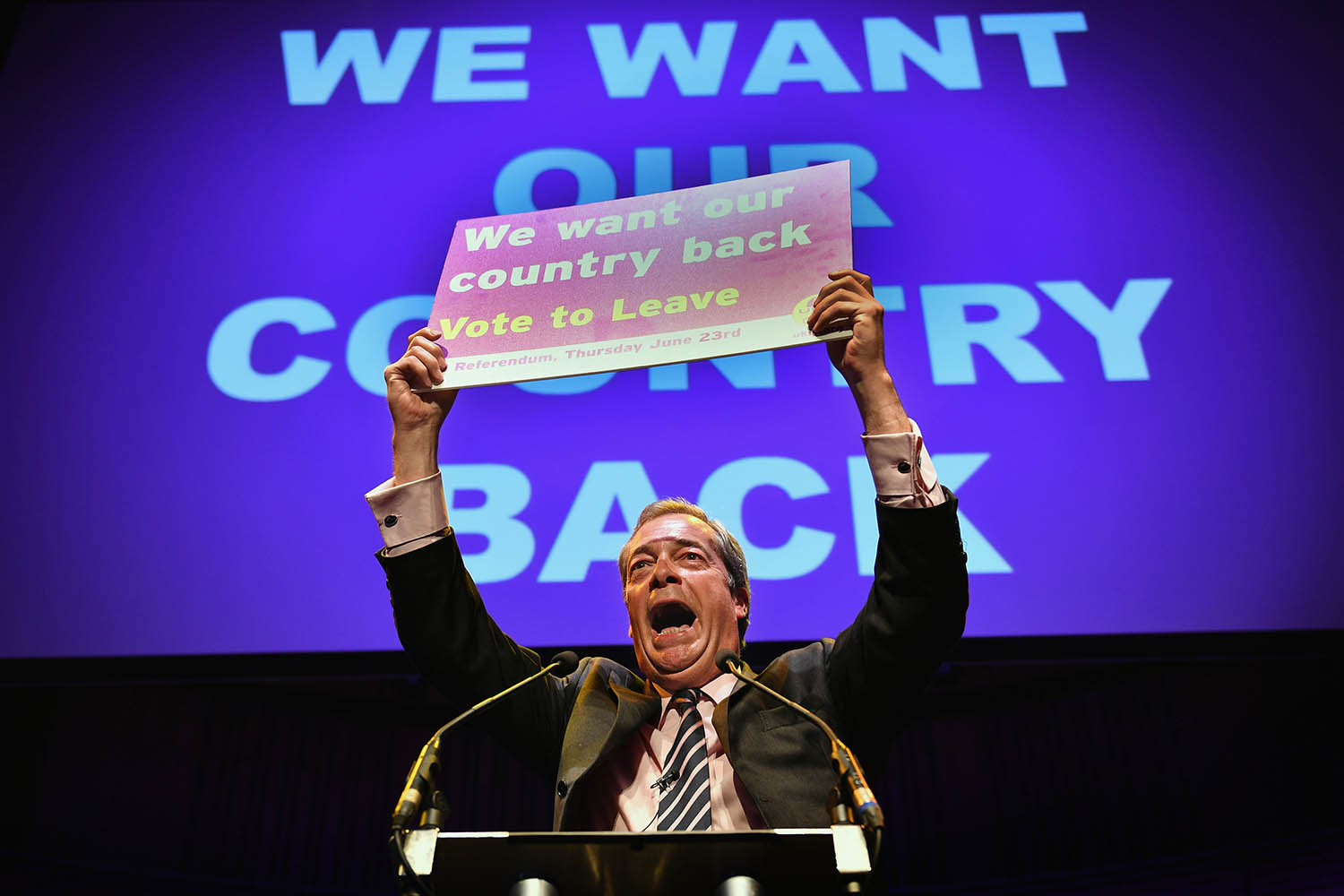

The deal is nowhere near as satisfying as re-entry to the single market and customs union would be, but it is better than nothing, and can be built on. Tearing it up would be, to mix metaphors, a retrograde step. And Thomas-Symonds points out that by opposing Labour’s recognition of the need to realign with Brussels, Nigel Farage “wants to take Britain backwards, cutting at least £9bn from the economy, bringing with it a risk to jobs and a risk of food prices going up”.

It is good that Thomas-Symonds is taking on Farage. I have been concerned for some time that Labour is running scared of Reform. One can certainly understand why. Over the past year, Starmer and his colleagues have seen Reform racing ahead in the polls and their own support collapsing. We now have a fissiparous political system in which the right is split between Reform and a desperate Conservative party, and the left between the government and the embryonic, nameless party of Jeremy Corbyn and Zarah Sultana.

But far from running scared of Reform, and aping its policies on migration, Starmer and his colleagues should tell it as it is.

And it is quite simple and obvious. Farage is a snake oil salesman. While capitalising, all too successfully so far, on the nation’s social discontent, he bears much of the responsibility for this discontent. Economists say exports are now running some 20% lower than they would have done without Brexit, and the annual loss to the nation’s output is put at 4% by the Office for Budget Responsibility and at more than that by the National Institute for Economic and Social Research and Bloomberg. That means more than £100bn a year off gross national product and about £40bn less in tax revenue.

As Michael Bloomberg said recently, Brexit is “the single stupidest thing any country has ever done”. And why did it happen? Essentially because prime minister David Cameron was – sorry! – running scared of Eurosceptics in general and Farage in particular. So he needlessly called the 2016 referendum, and we are now struggling with its consequences.

Starmer and Rachel Reeves were quite right to be unashamed remainers – and, for a time, rejoiners. They should have the courage of their previous convictions and ceaselessly point out that Farage cannot be trusted. Unlike Farage, they were right.

But we are where we are. The Bank of England governor, Andrew Bailey, has been warning about poor prospects for productivity and growth, plus unease about inflation. This is not unconnected with the damage caused by a decade of austerity and, yes, Brexit.

Now, one can hardly look at a newspaper or listen to casual pub talk without reading or hearing worries about the nation’s debt. But it is worth noting that, as Mario Draghi, former president of the European Central Bank, said recently, there is an important distinction between “good” and “bad” debt. Good debt is for investment that contributes to growth and productivity, and, far from “burdening” future generations, will almost certainly benefit them.

@williamkeegan

Photograph by Jeff J Mitchell/Getty Images

Newsletters

Choose the newsletters you want to receive

View more

For information about how The Observer protects your data, read our Privacy Policy